Title: Safeguarding Your Future: A Guide to Life Insurance

Introduction:

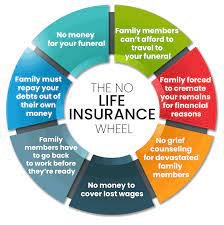

Life insurance is a crucial financial tool that provides a safety net for your loved ones in case of unforeseen events. Understanding the various types, benefits, and steps involved in obtaining life insurance is essential for making informed decisions about securing your family’s future. In this article, we’ll explore the world of life insurance in a reader-friendly manner.

Heading 1: The Basics of Life Insurance Subheading: Ensuring Financial Security for Your Loved Ones

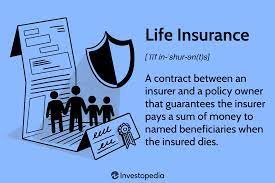

- Purpose: Provides a financial payout to beneficiaries upon the policyholder’s death.

- Types: Term life, whole life, and universal life are common categories.

- Coverage: Amount of money paid to beneficiaries is known as the death benefit.

Heading 2: Types of Life Insurance Policies Subheading: Choosing the Right Coverage for Your Needs

- Term Life Insurance:

- Provides coverage for a specific term, usually 10, 20, or 30 years.

- Generally more affordable but does not build cash value.

- Whole Life Insurance:

- Offers coverage for the entire lifetime of the policyholder.

- Accumulates cash value over time, providing a savings component.

- Universal Life Insurance:

-

- Provides flexibility in premium payments and death benefits.

- Combines life insurance with an investment component.

Heading 3: Determining Your Coverage Needs Subheading: Assessing Your Financial Responsibilities- Consider Dependents: Evaluate the financial needs of your dependents.

- Outstanding Debts: Factor in mortgage, loans, and other outstanding debts.

- Education Expenses: Plan for your children’s education costs.

- Income Replacement: Ensure your policy covers the replacement of your income.

Heading 4: Steps to Purchase Life Insurance Subheading: A Simple Guide for Policy Acquisition

- Assess Your Needs:

- Determine the coverage amount and type of policy that suits your situation.

- Research Insurance Providers:

- Compare offerings from reputable insurance companies.

- Get Quotes:

- Obtain quotes to compare premiums and coverage options.

- Undergo Medical Examination:

- Many policies require a medical examination for accurate underwriting.

- Read the Policy Terms:

- Understand the terms, conditions, and exclusions of the policy.

- Select Beneficiaries:

- Designate beneficiaries who will receive the death benefit.

- Pay Premiums:

- Regularly pay premiums to keep the policy active.

Heading 5: Comparative Analysis of Life Insurance Policies Subheading: A Table for Informed Decision-Making

Insurance Provider Term Life Whole Life Universal Life Additional Features Provider A ✓ ✓ ✓ Accelerated Death Benefit Provider B ✓ ✓ ✓ Cash Value Component Provider C ✓ ✓ ✓ Flexible Premiums Heading 6: Frequently Asked Questions About Life Insurance Subheading: Clearing Common Doubts

Q1: Can I change beneficiaries on my life insurance policy? A1: Yes, you can typically change beneficiaries at any time by contacting your insurance provider and updating the necessary documentation.

Q2: Is it possible to cash out a life insurance policy before death? A2: Whole life and universal life policies often accumulate cash value that can be accessed through policy loans or withdrawals, but it may affect the death benefit.

Q3: What happens if I miss a premium payment? A3: If you miss a premium payment, the policy may lapse or enter a grace period. Some policies offer options to reinstate lapsed policies with additional conditions.

Heading 7: Conclusion Subheading: Securing Your Legacy and Providing Peace of Mind

In conclusion, life insurance is a crucial aspect of financial planning that ensures your loved ones are protected in the event of your untimely demise. By understanding the types of policies, assessing your coverage needs, and comparing offerings from different providers, you can make informed decisions to secure your family’s future. Remember, life insurance is not just a financial product; it’s a thoughtful investment in the well-being of those you care about.

-